Viewpoints

LaserPro Exchange (Factsheet)

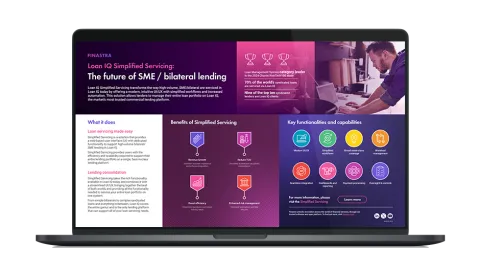

Loan IQ Simplified Servicing: The future of SME/bilateral lending

Trending

Finastra TV

FINANCE IS OPEN

Finastra TV is where you will be able to uncover the latest transformative trends shaping the world of finance and be inspired with insights from industry experts.