How banks and fintechs are learning to move fast, delight customers and innovate in today’s API-enabled economy

Just a few short years ago the mention of fintechs and financial institutions in the same breath was enough to silence any boardroom discussions. However, as we’ve all experienced over the past 12 months, the world of payments is changing rapidly and the ability for banks to embrace collaboration is now being seen as an essential approach to meet customer expectations and drive innovation. It is something that is redefining how banks approach designing new solutions.

2020 saw a number of high-profile examples hit the headlines, with Bank of America announcing its partnership with Ripple – as well as Google signing up six more partners for its digital banking platform. With many things being cited as ‘the new normal’, partnerships between banks and fintechs falls firmly into this category these days.

APIs used in banking were often proprietary tools in bank-specific systems. Back then, the only way for banks to collaborate with an external partner to drive innovation in payments was through point-to-point connectivity using bespoke links.

With today’s open APIs, things are very different. The collaboration environment has pivoted from a one-to-one model to one-to-many, with banks, fintechs and a wide array of other third-parties able to collaborate flexibly and seamlessly.

These opportunities are also now fostering a new way for banks to approach product design. Below are some examples.

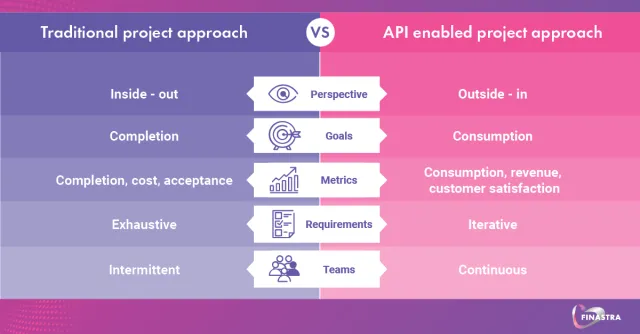

1. Taking an outside-in approach

At its core, an outside-in approach is about an obsession with the customer— i.e., relying on customer needs and preferences to guide product strategy. The outside-in perspective is data-driven and avoids making presumptions about customers but puts them front and centre and tests new ideas with them directly. The more traditional inside-out approach, in contrast, tends to either base strategies on the resources IT says are already available or on an internal presupposition about what developers and end users might want or need.

2. Improve time to market with MVPs

Previously banks assumed it is usually best to get to market with a fully functioning solution ready for all. This would lead to long development times and, once live, often see the solution as now obsolete. Embracing APIs, cloud and third party pilot programs using a minimum viable product (MVP) approach allows for rapid iteration and test and learn phases in a fraction of the time. Adopting a product mindset enables an organization to experiment with more ideas more widely and more quickly—and, as data comes in, to invest where products show promise and consider remediation where they don’t.

3. Rethinking monetization models

Monetization is an essential part of any business case and many API initiatives are started or funded based on the ability to monetize assets. This can come in many forms; reducing the cost of existing ‘analogue’ services, enabling the value of the data banks hold, and even savings seen with a rapid app development and prototyping approach should be considered. But sometimes even the ability to reach a customer through a new touchpoint enhancing acquisition and loyalty could earn you more in the long term.

As a result, a bank can harness a vast range of fintech-led innovation to deliver more compelling services and experiences to its customers, while also enabling its fintech partners to gain benefits – including access to the bank’s customer base and therefore the ability to enhance and extend their services.

Overall, the new collaboration model means that every banking product, third party or partner can extend its value by connecting with others via open APIs. This benefit applies whether the value is derived from utilizing payment processing services, increasing clearing reachability, or leveraging rich ISO 20022-derived data to increase automation and gain insights into customers’ behaviour.

Soon open APIs will power our financial lives too, driving comparative pricing apps, competition, new aggregated analytical tools and processing options as the banking sector continues to open up to them and recognize the value these new partnerships can bring to both sides. Authorized third parties can build products and data-rich services on top of existing applications by accessing open APIs. They effectively allow for a level playing field between banks big and small. Utilizing the expertise and resources outside of their own four walls and embracing new product approaches, as well as the new technologies that are making this possible, will help fuel competition and ignite innovation.

To learn more about the new era of open API innovation, download our white paper on Powering payments with open banking and APIs.