Powering the future of lending and corporate banking

Enabling financial institutions to accelerate innovation and deliver future-ready services across lending and corporate banking.

Discover how ING is revolutionising lending with the power of Finastra’s Loan IQ Nexus.

Watch nowThe trusted partner delivering modern lending and corporate banking software for institutions worldwide

Proven, trusted, secure

Backed by decades of global leadership, our solutions deliver reliability, compliance and operational resilience for institutions worldwide

End-to-end coverage across lending and corporate banking

Deliver comprehensive support from loan origination to servicing, trade finance, corporate channels and mortgage processing

Enhanced customer and borrower experiences

Deliver intuitive, seamless digital interactions that improve satisfaction and accelerate time to value

Multiple deployment options

Run your solutions on Finastra managed cloud, private cloud or on-premise environments, ensuring flexibility for institutions of every size and maturity

Modern, open architecture

Built on open APIs and standards-based integration, our platforms simplify connectivity across systems, automate processes and accelerate innovation across lending and corporate banking

Embedded AI to enhance productivity

Improve employee engagement and accuracy with built-in AI support and learning tools

Lending marketing solutions

Lending & Corporate Banking

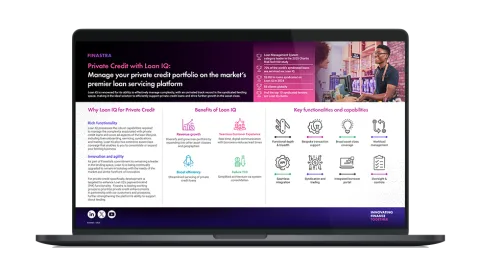

Finastra Loan IQ

Loan IQ is the market's leading loan servicing platform that can support the full spectrum of lending on a modern, unified platform.

Finastra LaserPro

Produce accurate loan documents faster with automated checks that reduce manual work, support compliance, and streamline commercial, consumer, and mortgage lending.

Finastra Trade Innovation

Transform trade operations with Trade Innovation a trusted booking engine that reduces manual errors, streamlines processing, and helps teams deliver accurate, compliant service.

Finastra MortgagebotLOS

Power mortgage originations with a secure LOS built for retail, wholesale, and correspondent mortgage loans while improving accuracy, speed, and compliance.

Finastra Originate Mortgagebot

Streamline the mortgage experience with an intuitive POS connected to MortgagebotLOS, guiding borrowers while helping you process applications faster.

ING + Finastra: Shaping the future of lending together

Discover how ING is revolutionising lending with the power of Finastra’s Loan IQ Nexus

The bank has made significant progress in its adoption of Loan IQ.

We are almost on 95% of the portfolio being on Loan IQ. That gives a big leverage when it comes to having one way of consolidating the data, which is very key for the next journey.

Our lending solutions are geared to support your growth

Explore our lending and corporate banking portfolio

Opening the doors of opportunity

Simplifying & automating processes while improving borrower experience.

Innovations that bring handshakes

Comprehensive end-to-end loan management solutions

Build deeper customer relationships

Bring new opportunities to life

Complete loan lifecycle management systems

Comprehensive functionality

Loan management software that reduces costs and brings efficiencies.

Streamlining operations

A digital experience that reduces manual intervention and, therefore, risk and human error.

Better customer experience

A smoother onboarding experience that helps attract and retain customers.

Featured Apps

CredAble

ClearTrade

CoriolisESG

FinverityOS

Additional resources to support your success

Lending FAQs

Talk to us about your lending needs

Simplifying and automating processes while improving borrower experience.