Ready to monetize? How to turn open banking APIs into bank revenue

What started as an open banking compliance requirement has evolved into a broader open finance opportunity, becoming one of the most important drivers of growth in modern financial services. Banks now sit in an environment influenced by fintechs and big tech platforms, competing for customers who expect speed, personalization, and frictionless digital access.

In this landscape, open banking application programming interfaces (APIs) have become far more than technical connectors; they act as commercial enablers for banks to extend their services, integrate with ecosystems, and unlock new bank revenue opportunities. As financial institutions (FIs) look for sustainable growth, APIs serve as a core business strategy that simultaneously elevates traditional IT architecture.

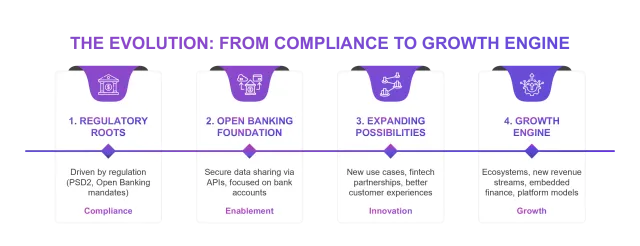

From compliance to revenue: The open banking API opportunity

The early phase of open banking was driven largely by regulation, focused on standardization, access to data, and mandatory interoperability. While that foundation remains important, the conversation has now evolved. Today, leading banks see APIs as commercial assets that can generate value across multiple channels. In fact, over 85% of banks worldwide have already adopted open banking APIs.1

This shift reflects growing pressure on traditional bank revenue models. Margins fluctuate, fee structures face scrutiny, and customer acquisition costs continue to rise, and, at the same time, digital-native competitors bring faster, more flexible services to market. Within this context, banks are rethinking how value is created.

APIs empower FIs to broaden their service opportunities while also participating in wider digital ecosystems, which transforms connectivity into opportunity and allows them to move beyond internal efficiency gains and into external revenue generation.

What we’ve seen in the past is that early movers in API strategy gain a competitive advantage. They establish relationships with fintechs and ecosystem partners earlier, build reusable infrastructure, and create scalable distribution channels that support long-term growth.

What API monetization means for banks today

API monetization refers to the process of generating value from APIs, either directly through pricing models or indirectly through expanded product reach, improved efficiency, and enhanced customer engagement.

In practical terms, monetization takes many forms. Banks can charge for API access, bundle services into subscription offerings, or enable partner-driven distribution models that expand usage across new customer segments. Value then emerges through more transaction volumes, reduced acquisition costs, or improved cross-sell opportunities.

Bank and fintech partnerships play a central role in this ecosystem. By working with fintech partners, banks can embed their services into third-party applications, marketplaces, and digital platforms, which creates new customer entry points without requiring banks to build and maintain every front-end experience. APIs also allow banks to reposition themselves within value chains. By evolving from isolated service providers into active platform participants, banks enable others to build on top of their infrastructure. This repositioning expands their reach while maintaining control over core financial capabilities, compliance, and risk management.

Revenue models that turn APIs into profit

To generate revenue from APIs, third parties need access to financial services such as payments, lending or data analytics. These APIs then act as scalable systems that provide operational capabilities beyond traditional bank revenue models.

API-driven revenue strategies typically fall into several categories, each supporting different business objectives and levels of maturity.

- Transaction-based pricing remains one of the most common bank revenue models. Banks generate revenue each time an API is called or a service is used. This specific model aligns pricing with usage, making it scalable and flexible for banks and their partners.

- Subscription-based models offer tiered access to APIs based on usage levels, feature sets, or service bundles. This approach creates predictable revenue streams while encouraging long-term, mutually-beneficial bank and fintech partnerships.

- Revenue-sharing models are increasingly popular in ecosystem-driven environments. Here, banks collaborate with fintechs and other partners to co-deliver services, sharing income generated from end-user transactions or product usage. This structure is particularly favorable when it comes to distributing commercial risk.

Together, these models contribute to more diversified and resilient bank revenue streams. They also encourage banks to think more strategically about how services are packaged and consumed across digital channels.

Scaling fintech partnerships through APIs

APIs play an important role in scaling fintech partnerships by simplifying integration, reducing onboarding friction, and enabling faster time-to-market. Banks can scale fintech partnerships, reduce onboarding friction, and achieve a faster time-to-market by offering standardized interfaces that support repeatable, scalable collaboration and bypass traditional operational complexity. Fintech partners gain access to regulated financial capabilities, while banks benefit from their agility and access to new customer segments.

An effective ecosystem strategy often requires more than technical connectivity. It also depends on governance frameworks, clear onboarding processes, and consistent developer experiences. When these elements align, banks can create environments where innovation happens continuously rather than in silos. Over time, API-driven ecosystems become self-reinforcing, with each new partner capable of expanding distribution, growing usage and strengthening the platform’s overall value proposition.

Banks must also choose the right technology platforms and partners. In the case of ecosystem partnerships, read our take on how orchestrators can ensure vision alignment from the start.

Use cases driving growth with open banking APIs

Several high-impact use cases demonstrate how value is being created through open banking APIs in real-world environments. Embedded finance is among the most transformative. Financial services are increasingly integrated into non-financial platforms, allowing customers to access lending, payments, and accounts directly within the applications they already use. In the US alone, 52% of adults now use at least one open banking-enabled service, such as a budgeting app, payment platform or lending tool.1 Leveraging this access is an opportunistic way to increase convenience while driving higher transaction volumes for banks.

Payments are another major growth area. Open banking APIs enable real-time payment initiation, improved reconciliation, and seamless integration with digital commerce platforms, helping banks stay relevant in fast-moving digital payment ecosystems.

Open banking API innovation also drives change in the lending market. Faster data access and automated decisioning processes allow banks to deliver more responsive credit products, improving both customer experience and approval time. In many cases, this leads to higher conversion rates and expanded lending portfolios.

Competing with big tech through platform banking

Big tech companies have reshaped customer expectations by delivering seamless, data-driven experiences across multiple services. Their strength lies in ecosystem design, where users can access payments, commerce, communication, and content within a single digital environment.

Banks respond to this shift through platform banking models that integrate financial services into broader digital ecosystems. They secure their presence in customer journeys that extend beyond traditional banking channels by embedding services within third-party platforms, super apps, and partner ecosystems.

Platform banking relies heavily on APIs as the underlying infrastructure. Without secure and scalable open banking API architectures, integration with external ecosystems becomes slow and expensive. With them, banks can participate more effectively in digital value chains and respond more quickly to changing market dynamics.

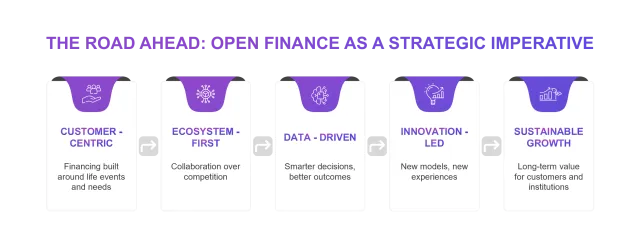

Building the foundations for API-driven revenue growth

As open banking continues to evolve, the importance of APIs only strengthens. They now sit at the center of modern financial ecosystems, enabling banks to connect services, share data securely, and deliver seamless digital experiences. Next-gen banking is becoming essential in this environment, where customers expect real-time access and personalized experiences. To meet their demands, FIs need technology foundations that support agility and innovation.

Finastra’s digital banking solutions are designed to help banks meet these exact demands. Finastra Essence is our next-gen core banking solution that combines broad and deep banking functionality with advanced technology capabilities. Built around five key elements - digital to the core, composable banking, actionable insights, cloud from the inside out, and a platform for innovation - the solution helps banks modernize operations while supporting API-driven business models and ecosystem connectivity.

Alongside this, Finastra Essence Analytics helps FIs transform raw banking data into actionable insights, predictive models, and an AI-ready analytics foundation. As banks continue expanding API ecosystems and digital partnerships, the ability to generate meaningful intelligence from data becomes increasingly valuable for improving decision-making, customer engagement, and operational performance.

Together, these capabilities provide a strong foundation for banks looking to scale innovation, strengthen ecosystem participation, drive bank revenue, and unlock long-term growth opportunities.

Sources:

1. CoinLaw. (2026) ‘Banking API Statistics: 2026 Market Size, Adoption, and Growth’. 2026. Available online at: https://coinlaw.io/banking-api-statistics/

Written By